Tata Motors: Driving in Reverse Gear

08-Sep-15 Leave a comment

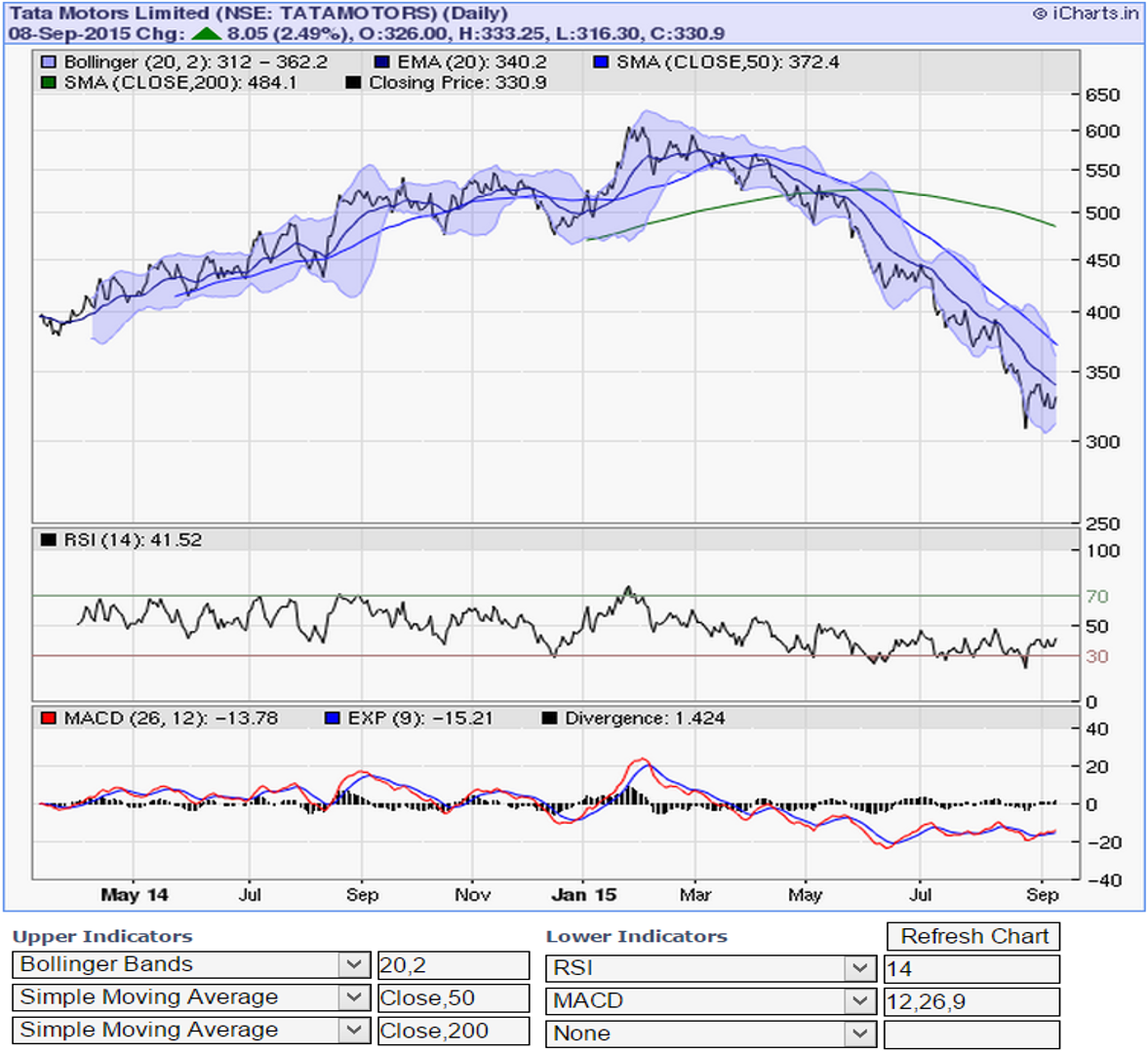

The stock of Tata Motors has fallen ~45% in the last 7 months! That’s a big drop for a big company. The stock’s around 10 times it’s trailing 12 months’ earnings. Upstarts like Flipkart are getting valued more than Tata Motors. That’s surprising. Is it about the unattractiveness of the business of making cars or is it a case of over-valuation of ecommerce businesses or is it both? Tata cars are everywhere, including China. It’s quite a venerable brand not to have a Peter Lynchian roadhead moment on:

The stock of Tata Motors has fallen ~45% in the last 7 months! That’s a big drop for a big company. The stock’s around 10 times it’s trailing 12 months’ earnings. Upstarts like Flipkart are getting valued more than Tata Motors. That’s surprising. Is it about the unattractiveness of the business of making cars or is it a case of over-valuation of ecommerce businesses or is it both? Tata cars are everywhere, including China. It’s quite a venerable brand not to have a Peter Lynchian roadhead moment on:

I am a hard working taxi driver and I have seen my share of cabs and cars (mostly cars that looked like cars) and have even heard of some feline roadhogs (read Jaguars) and then my last passenger told me about this massive 45% drop in the share price of the company that makes these things. I have this Peter Lynch moment and I want to buy this stock.

It’s the crumbling of the Chinese walls that is a part of the reason why the stock’s down. Cool Chinese have been doing uncool things like not buying Jaguars as much as they used to earlier. Things have been very bad for the company during the last couple of quarters. So bad that they chose to raise capital via a rights issue. That’s a sure shot sign of severe financial stress. Worse, the stock price kept of falling leaving the rights price level far behind. And then the unkindest cut was the skipping of dividend by the folks that run this rather complex business.

But then I am a surfer. An opportunist and a speculator. I am rooting for a 35% return on this idea.

Here’s some pointers to mull over:

- Commodity prices have hit rock bottom. Cars require a lot of metal to make. Should be cheaper to build a car. Selling them is a totally different matter altogether!

- Valuation is attractive. Trailing 12 months’ P/E of around 10.

- Stock’s corrected 45% now from 7 months back

- The technicals don’t scream a buy, but are giving a very strong hint. The next few days price action should confirm.

- We can (and should) forgive the management for skipping dividend for the first time in 15 years. That’s so unlike a Tata. A black swan Tata, perhaps.

- We can (and should) ignore the fact that the management seems to have pulled off an opportunistic rabbit from the (minority) shareholders hats by pricing the recent rights issue at 450.

Recent Reactions