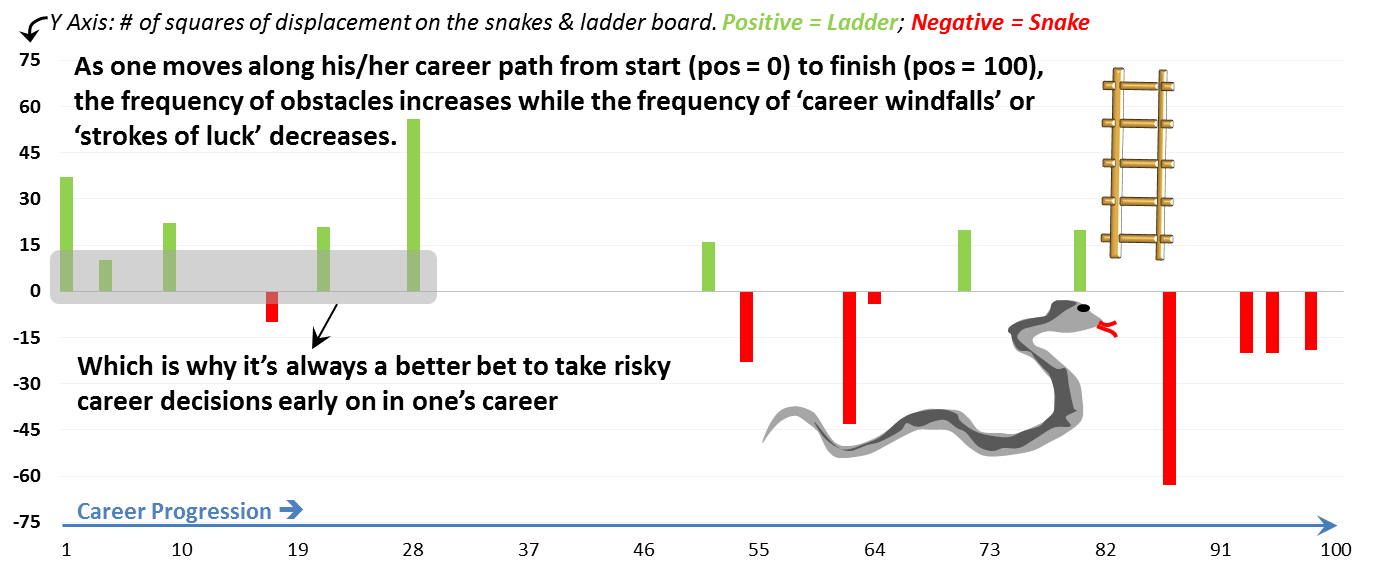

Your Paths to Success in your Career

04-Jan-14 1 Comment

This is how some people plan their careers:

This is what actually happens:

04-Jan-14 1 Comment

This is how some people plan their careers:

This is what actually happens:

13-Oct-10 2 Comments

In my post titled Portrait of a Portfolio, I had talked about my conscious shift towards a higher frequency of trading since the start of this calendar year. A lot many informed voices were then pointing out to increasing choppiness and therefore the need to be nimble and hit the right spots in terms of stock selection. The standard ham was “India is a growth and domestic consumpition driven story – long term trajectory remains upwards – but there is a lot of pain in the international markets – higher volatility is expected – cannot predict what the market will do by end of 2010 but stock specific action will abound”. Since I personally agreed to this prognosis and also since a relatively high frequency style of trading/investing suits my personality, I applied this mantra not just to that Portfolio I talked about on 7Oct’10, but to the entire block of personal capital that I ‘play’ with.

A natural consequence of the rapid churing out of my positions is a sharp reduction in the average holding period of my trade positions. These days I have been holding my positions for an average of 45 – 60 days only! This is in stark contrast to the 500+ days positions I normally used to have prior to the crash of the previous year. So, as part of the ongoing effort to gather insights on the best method of selling out, I tried to look at the relation between the returns that I have earned and the time I have spent in nurturing my trades. I took all the 306 odd closed trades that I have on me since May’03 and tried to stack up the (weighted) average returns across the corresponding holding period in calendar days. The chart shown on the right is what came about. The picture in inset shows the same chart with the full range of the y-axis (representing % returns) – I could not resist blowing my trumpet on the 18 bagger investment of mine which I held on for a good 978 calendar days. It was not a black swan – though it is an outlier on the chart – there was logic and conviction backing that trade all the way. I really don’t know if it’s just poor me or even other market players are currently feeling that the age of finding such skyscrapers has passed us by. Anyways, the main body of the chart is squeezed into a narrower vertical range to bring out more detail on the other trades.

A natural consequence of the rapid churing out of my positions is a sharp reduction in the average holding period of my trade positions. These days I have been holding my positions for an average of 45 – 60 days only! This is in stark contrast to the 500+ days positions I normally used to have prior to the crash of the previous year. So, as part of the ongoing effort to gather insights on the best method of selling out, I tried to look at the relation between the returns that I have earned and the time I have spent in nurturing my trades. I took all the 306 odd closed trades that I have on me since May’03 and tried to stack up the (weighted) average returns across the corresponding holding period in calendar days. The chart shown on the right is what came about. The picture in inset shows the same chart with the full range of the y-axis (representing % returns) – I could not resist blowing my trumpet on the 18 bagger investment of mine which I held on for a good 978 calendar days. It was not a black swan – though it is an outlier on the chart – there was logic and conviction backing that trade all the way. I really don’t know if it’s just poor me or even other market players are currently feeling that the age of finding such skyscrapers has passed us by. Anyways, the main body of the chart is squeezed into a narrower vertical range to bring out more detail on the other trades.

Some interesting observations and takeaways come about. I guess, some of these might be applicable to you as well since like it or not us amateurs seem to be cut from the same cloth:

17-Aug-10 5 Comments

Many investors err when they end up throwing good money after bad. The temptation to average the costs down has weighed down on most of us. The problem with this tactic is that it works only when you have studied the underlying asset very very thoroughly. Most of us do not do this. Most of us are not equipped to do this. Most of us do not have the time nor the patience to do this. The other mistake that many investors make is that they get into a position without having pre-decided their stop losses. Or ignoring the stop losses when confronted with a losing proposition.

Many investors err when they end up throwing good money after bad. The temptation to average the costs down has weighed down on most of us. The problem with this tactic is that it works only when you have studied the underlying asset very very thoroughly. Most of us do not do this. Most of us are not equipped to do this. Most of us do not have the time nor the patience to do this. The other mistake that many investors make is that they get into a position without having pre-decided their stop losses. Or ignoring the stop losses when confronted with a losing proposition.

Almost all of us would have had someone in our extended family or friend circle who might have been badly mauled by the markets and would have consequently vowed never to return. It’s not their trades or the risky nature of the markets that did them in. It’s their lack of discipline. So many times we hear the refrain that markets are too risky. Actually, the market is not risky at all – it is the behaviour of the investor that is risky. The market never induces you to buy. This weekend when I was in Bombay, my mother told me about the losses that my father had totted up during his investing misadventures. Luckily for us (my brother & I) he did not sell off his losses, he just ignored them. And these shares (most of them cyclicals) passed on to us after his demise. And wow! The cycle turned in 2002/03 and how! Imagine riding Steel Authority of India Limited from 6 to42 in a period of 18 months. That hooked me for life. Till the losses tested me.

Almost all of us would have had someone in our extended family or friend circle who might have been badly mauled by the markets and would have consequently vowed never to return. It’s not their trades or the risky nature of the markets that did them in. It’s their lack of discipline. So many times we hear the refrain that markets are too risky. Actually, the market is not risky at all – it is the behaviour of the investor that is risky. The market never induces you to buy. This weekend when I was in Bombay, my mother told me about the losses that my father had totted up during his investing misadventures. Luckily for us (my brother & I) he did not sell off his losses, he just ignored them. And these shares (most of them cyclicals) passed on to us after his demise. And wow! The cycle turned in 2002/03 and how! Imagine riding Steel Authority of India Limited from 6 to42 in a period of 18 months. That hooked me for life. Till the losses tested me.

It does not matter when you buy, it’s when you sell that’s most important. This post is one amongst the various efforts on my part to understand the full meaning of this sentence as per my 5Aug resolution. One can get out of a position making a profit or else leave the table with a loss. Stop losses are signposts that help you decide when to sell if your trade does not work out the way you intended it to be. There’s no emotion involved, just hard  nosed, dispassionate, stoic discipline. Statistically, mostly men/boys invest – so much so that investing might seem like a male thing to do. But successful investing is really quite machinistic and dull. Stick to one trading system, do not flip in and out. Stick to your stop losses. Write down/visualise your goals for each position. Maintain a trading journal recording your behaviour and why you did what you did kind of thing. Boring. Please read this cool article which talks about the 5 uncommon rules of the really wealthy traders to get some sense of how boring trading can get! Putting money in a bank fixed deposit or better still a ULIP can be so exciting! You’d get all the time in the world to party.

nosed, dispassionate, stoic discipline. Statistically, mostly men/boys invest – so much so that investing might seem like a male thing to do. But successful investing is really quite machinistic and dull. Stick to one trading system, do not flip in and out. Stick to your stop losses. Write down/visualise your goals for each position. Maintain a trading journal recording your behaviour and why you did what you did kind of thing. Boring. Please read this cool article which talks about the 5 uncommon rules of the really wealthy traders to get some sense of how boring trading can get! Putting money in a bank fixed deposit or better still a ULIP can be so exciting! You’d get all the time in the world to party.

Sometime back I saw the movie Kites. Kabir Bedi, a powerful casino owner plays the father of Nick Brown who tells this to his revenge driven son when the woman whom he was to marry elopes with Hrithik Roshan:

“The true gambler is the one who knows when to get up from the table”

The other anecdote that comes to mind is from a job interview that I had conducted for a senior position in my company some time back. The candidate was trading on the prop account of some agency and among other questions I had asked him about his trading style and attitude towards stop losses. The guy said that he had never ever violated his stops. The two people who reported in to him had busted their stops one time each. I don’t care if this was just for the effect but inspiration strikes from the most unlikely of places. I have read quite a few books on trading, psychology of trading but when I met this “pretending to be in control” guy I thought that if this chap can do it, why can’t I. I’ve respected my stops ever since – hopefully it will become a habit.

This is important since stop losses can protect you even if you suddenly get whiplashed by a sharp correction. In fact its quite cool since you will quickly be in cash and hopefully will be able to redeploy and make more than what the stops cost you. Which brings me to important question: What should the ideal stop loss be?

The quantum of stop loss depends on what you expect from your investments and who you are. If you trade in and out intra-day (the post is not meant to be read by such people anyways) then your stop loss levels will obviously be extremely tight. Maybe 1% – 2%? There’s a lot of material on discussion forums and websites which points out to 2% being a good rule of thumb. But I feel that if one trades for longer periods, across multiple settlement periods a level of 5% is good enough. The volatility in Indian stocks is high enough to justify a 5% stop loss level. This point is important since if you are an infrequent trader then there is a danger of getting whipsawed if you put too tight a stop. Putting too tight a stop is like writing an annuity cheque to your broker. Your choice of stop loss ideally should be predicated by:

Mental stops do not work. Period. I have done some conditional formatting and alerts on my trading spreadsheet and the annoying things keep popping up reminding me to cut my losses and run. You could have your own custom system, more sophisticated than mine, but do not do it only in the mind. It’s easy to overrule one’s mind.

This piece is obvisouly written for people like me. Casual traders. Folks that have a day job and who can afford to look at stock prices only a couple of times a week when the market is on and perhaps 3 – 4 times a week at night while the market sleeps. Folks who want to flog their investible surplus for some alpha instead of letting it rot in bank deposits. The Anirudh Sethi Report, which incidentally became the first site to link to my website has a cool example of how stop losses can be used to make money a la big game shooting. The lesson is almost like a Zen Koan. In fact, Zen masters would make awesome traders.

11-Aug-10 1 Comment

The US President is going around asking his fellow countrymen to produce more graduates and compete with the likes of India and China. These are good points to raise but then when this is accompanied by curbs on granting visas it begins to sound like rhetoric. All under the guise of protecting US borders! The border security bill will hike visa fees to $2,000 per applicant for companies that have fewer than 50% of its workforce as US citizens. Thats a cool $200 million bill for Indian software companies that rely heavily on “body shopping”. The standard line of the Indian industry has been a lament on the lack of the totalisation pact between the two countries. India has to contribute towards social security for the workers that it sends to the US – and if they return back to India, there is no possibility of a refund. I would welcome to hear something from Dr. Manmohan Singh on the issue. He is his usual quiet self.

The US President is going around asking his fellow countrymen to produce more graduates and compete with the likes of India and China. These are good points to raise but then when this is accompanied by curbs on granting visas it begins to sound like rhetoric. All under the guise of protecting US borders! The border security bill will hike visa fees to $2,000 per applicant for companies that have fewer than 50% of its workforce as US citizens. Thats a cool $200 million bill for Indian software companies that rely heavily on “body shopping”. The standard line of the Indian industry has been a lament on the lack of the totalisation pact between the two countries. India has to contribute towards social security for the workers that it sends to the US – and if they return back to India, there is no possibility of a refund. I would welcome to hear something from Dr. Manmohan Singh on the issue. He is his usual quiet self.

While India remains preoccupied with flash floods, Kashmir, honour killings and the Commonwealth Games tamasha, China picked up the gauntlet and responded well by making outsourcing completely tax free if delivered from 21 cities. The Chinese have made no bones about the fact that they want to end India’s dominance in the sector. Should India not make a counter move to steal some foundries away from China?

India’s earlier responses sound quite pathetic to me. If the US politicians are ushering their wards back to school and hoping and helping their middle class to retain their sources of income, whats wrong with it? Cribbing about it and making it sound as if some grave injustice is being done against it is mooching. How would India feel if people across its eastern border arrived in hordes and stole away jobs? Some factions cannot even tolerate intra country movement of labour.

The rhetoric in the US however is also missing its mark. Senator Charles Schumer has called Infosys a chop shop. Its easy for the sound bytes to morph into an India/China hate undercurrent (if one does not exist already). Lou Dobbs, a popular media anchor, for instance has written a book on outsourcing and devotes much of his website to the phenomenon and how the American middle class is being killed. Is it? Don’t think so. Maybe going through a very tough phase. An important counterpoint to note is the indirect benefit that this can yield to the US.

It would be good for the US to note that the Indian middle class is gravitating towards more and more consumerism. People are seeing their incomes rise and are swiping their credit cards, buying second houses, ipods, etc. gleefully. This is allowing banks like BoA, Citibank etc to set up their shops in India. While such benefits selectively accrue to the Dells, Microsofts and BoAs of the world, the American middle class can certainly benefit. President Obama should also consider exhorting his masses to match imports (of services from China and India) with American exports to these countries. The oriental appetite for consuming intelligently designed goods and services in the occident will only grow. Americans would do well to understand one basic trait of most Indian middle classes – they are afraid to take risks. Innovation is rarely seen. While hordes of software junkies pound away at maintenance and basic software jobs, there is hardly any technological breakthroughs that emerge from this populous nation. The US has always thrived by managing risk and employing innovation which have set up a very strong financial acceptance to see capital freely flowing to fund ventures that are risky. Indians generally take the easy way out – outsourcing is one of them.

It would be good for the US to note that the Indian middle class is gravitating towards more and more consumerism. People are seeing their incomes rise and are swiping their credit cards, buying second houses, ipods, etc. gleefully. This is allowing banks like BoA, Citibank etc to set up their shops in India. While such benefits selectively accrue to the Dells, Microsofts and BoAs of the world, the American middle class can certainly benefit. President Obama should also consider exhorting his masses to match imports (of services from China and India) with American exports to these countries. The oriental appetite for consuming intelligently designed goods and services in the occident will only grow. Americans would do well to understand one basic trait of most Indian middle classes – they are afraid to take risks. Innovation is rarely seen. While hordes of software junkies pound away at maintenance and basic software jobs, there is hardly any technological breakthroughs that emerge from this populous nation. The US has always thrived by managing risk and employing innovation which have set up a very strong financial acceptance to see capital freely flowing to fund ventures that are risky. Indians generally take the easy way out – outsourcing is one of them.

But these shifts and changes, as significant as they can be, happen slowly and the threat of the current American middle class losing its plot somewhere is indeed very real. And such Obama speak will found many takers and therefore votes. Whether the White House politicians actually act in earnest to plug the leak (which in my opinion they should not blindly do) is a different matter. Donations from many top industry groups may be funding the election expenses of these law makers.

In my opinion, its futile for the US (as a nation and culture) to fight outsourcing. Its perfectly logical and sane for the US society to agitate and therefore equally logical for the politicians to flog this sentiment for election victories. The US should focus on earning export dollars (USD should depreciate as years roll by) by tapping into the growing prosperity in China and India. India and China, on the other hand, should open up their economies further, slicing and selling off non-strategic assets to the highest bidders and generating more wealth in the process. Its a great lifetime to spend in the Indian and Chinese capital markets of today.

In my opinion, its futile for the US (as a nation and culture) to fight outsourcing. Its perfectly logical and sane for the US society to agitate and therefore equally logical for the politicians to flog this sentiment for election victories. The US should focus on earning export dollars (USD should depreciate as years roll by) by tapping into the growing prosperity in China and India. India and China, on the other hand, should open up their economies further, slicing and selling off non-strategic assets to the highest bidders and generating more wealth in the process. Its a great lifetime to spend in the Indian and Chinese capital markets of today.

{kind=link}

Recent Reactions