A deluge of work kept me away from the keys momentarily. As I had said in some of my previous posts, I am massively long Godrej Industries Limited. While the stock has moved up quite a bit since my first post on it dated 11Jul’10 it did give back some 13% of its gains during the previous 45 days or so. I am perfectly happy with the situation. The position is net up 34% (weighted average) for me over the past 5 months that I’ve been holding it. I guess I was lucky to have bought into it at a good time and from here on I am content for it to give me a slow and steady compounding. In fact the purchase logic was based on the diversification that GIL gives – given it’s 69.4% and 23.4% holding in Godrej Properties Limited (GPL) and Godrej Consumer Products Limited (GCPL) respectively (and other group companies). Of course, there is the native chemicals business of GIL as well . While holding companies will never trade at a sum predicated by the value of their assets, the beta reduces as compared to a direct exposure to GPL. In the case of holding companies, the sum of parts is always less than the whole.

A deluge of work kept me away from the keys momentarily. As I had said in some of my previous posts, I am massively long Godrej Industries Limited. While the stock has moved up quite a bit since my first post on it dated 11Jul’10 it did give back some 13% of its gains during the previous 45 days or so. I am perfectly happy with the situation. The position is net up 34% (weighted average) for me over the past 5 months that I’ve been holding it. I guess I was lucky to have bought into it at a good time and from here on I am content for it to give me a slow and steady compounding. In fact the purchase logic was based on the diversification that GIL gives – given it’s 69.4% and 23.4% holding in Godrej Properties Limited (GPL) and Godrej Consumer Products Limited (GCPL) respectively (and other group companies). Of course, there is the native chemicals business of GIL as well . While holding companies will never trade at a sum predicated by the value of their assets, the beta reduces as compared to a direct exposure to GPL. In the case of holding companies, the sum of parts is always less than the whole.

The quartely results of GIL were announced on 27Oct’10. The net profit on a QoQ basis increased by 12.5%; their chemicals and agri business is looking up and other regulation stuff. Nothing much to write home about the results – along expected lines of the company and the analysts. There was an expressed fear about inflaton eating into the profits of GCPL but that did not happen. The possible hardering of the interest rates could eat into the margins of consumer durables industry though which is generally believed to be a rate sensitive sector like auto. That remains to be seen.

I keep tracking the news stories about GIL fairly regularly. The company has certainly kept the news wires busy in the past months. I don’t know why but I end up investing in companies which use Bollywood and regional film personalities to peddle their products. A lot of names have been coming up in my alerts on GIL – the likes of Raveena Tandon, Soha Ali Khan, Vijayalaxmi, Malaika Arora Khan, Vidya Balan, Mugdha Godse et al. The other company whose products are endorsed by stars is Gitanjali Gems, which is now up a further 10% since my last post on it dated 25Oct’10. Cool. Here are some other important news stories that I caught re Godrej Industries:

– The new Godrej Appliances ad tries to shift the customers’ focus from refrigerators to other white goods. The company sells one fridge every 30 seconds in India so they’re correct in spending ad money on stuff other than fridges. The other good thing about the ad is that it does not feature Preity Zinta – which is a good change, according to me!

– Godrej Agrovet is exploring acquisitions in micro irrigation (competition for my other position in Jain Irrigation?). The prime minister shook a lot of hands in Malaysia recently – maybe that bodes well for Godrej Agrovet’s palm oil business?

– I keep the Godrej hand sanitiser (Protekt) at my work place. It’s good. This market (currently at 25 – 30 crores only) is growing at 50% per annum and is in its infancy. GCPL is eyeing a quarter of this pie.

– GPL expects it’s revenues to rise 50% this fiscal. There have been a few assorted stories saying that realty stocks will fall since the RBI has come out with tougher norms for bank lending to the housing sector. I don’t subscribe to that view. Point being, first time home buyers can always borrow the additional 5% – 10% from family while older home buyers should have the necessary funds. In any case, 1) GPL wants to increasingly focus on affordable housing in cities like Nagpur and Kanpur – where the demand should continue to remain high and 2) some banks were anyways calculating the % of finance at 85% of property value+ stamp duty. There is a tremendous ambition in smaller towns to go upscale and improve the quality of lives – and GPL should benefit. There is another company called Ashiana Housing Limited – which looks reasonably priced and is also following the joint venture model of GPL. Need to check on that story. But later.

– They’re looking to merge GCPL with Godrej Household Products Ltd (GHPL). GCPL is keen on acquiring FMCG firms, particularly in hair colouring, household insecticide and personal wash segments in Asia, Africa and South America. Good luck on that. The proces of consolidation will show whether GCPL can truly make itself over into a true multinational with a common footprint across multiple countries rather than merely being a company with a motley collection of stakes in various companies across the occident and the dark continent.

– Close to 80% of construction of GPL will be for residential purposes. Thankfully, we need not worry about SEZs and other commerical sales, which are highly correlated to business environment. The good thing about GPL (had mentioned in previous posts) is that it just wants to focus on its core area of expertise – getting the projects, the JVs with land owners, marketing and sales and using its brand pull to get in the home buyers.

– While the focus is on affordable housing in the 25 lakh bracket, GPL also has its game right in the mecca of big property in this country: Bombay. The story about it’s gigantic plot of land in Vikhroli is old hat. What’s new is the JV with Bombay Footwear to develop 1.5 lakh sq ft in Chembur and a MoU with Jet Airways to deliver 1 million sq ft of office space in Bandra Kurla Complex.

Mutual funds have been on a selling spree while the Foreign Institutional Investors lap up our desi shares. GIL however has been on the buy list of the fund houses like DSP, Edelweiss, HDFC and Religare. I am ready to load up more on my already massively long, passively managed position but it needs to dip down (on unrelated news). Till such time I will have to keep suffering Preity Zinta I guess. Cheers.

Please scatter it around:

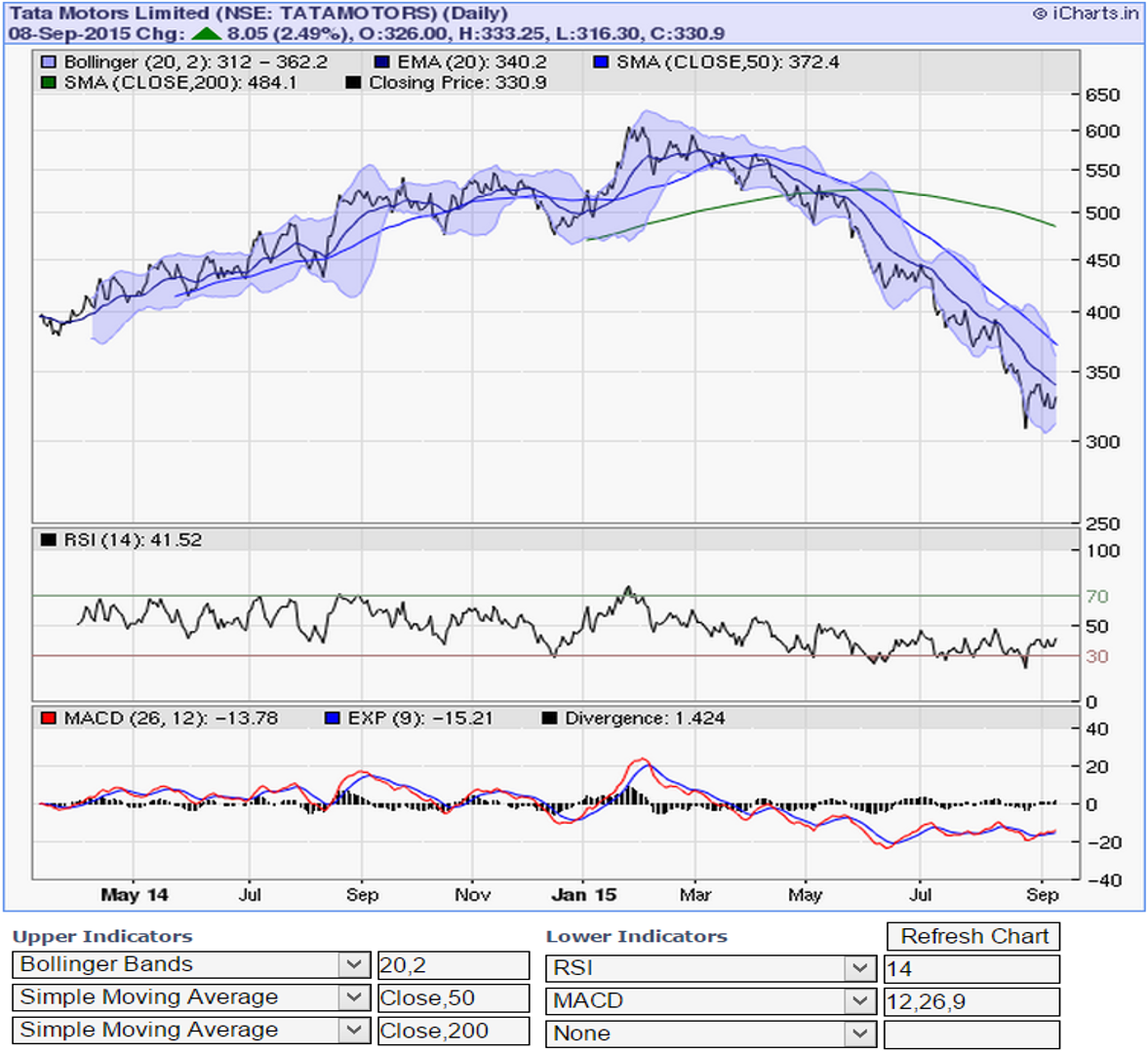

The stock of Tata Motors has fallen ~45% in the last 7 months! That’s a big drop for a big company. The stock’s around 10 times it’s trailing 12 months’ earnings. Upstarts like Flipkart are getting valued more than Tata Motors. That’s surprising. Is it about the unattractiveness of the business of making cars or is it a case of over-valuation of ecommerce businesses or is it both? Tata cars are everywhere, including China. It’s quite a venerable brand not to have a Peter Lynchian roadhead moment on:

The stock of Tata Motors has fallen ~45% in the last 7 months! That’s a big drop for a big company. The stock’s around 10 times it’s trailing 12 months’ earnings. Upstarts like Flipkart are getting valued more than Tata Motors. That’s surprising. Is it about the unattractiveness of the business of making cars or is it a case of over-valuation of ecommerce businesses or is it both? Tata cars are everywhere, including China. It’s quite a venerable brand not to have a Peter Lynchian roadhead moment on:

Recent Reactions